Retirement feels close when markets stop cooperating

The last few years can feel oddly compressed: a retirement date looks “basically here,” but the account balance refuses to hold still. A 12% drop doesn’t read like a line on a chart anymore; it’s a delayed kitchen remodel, a second look at health insurance, a quieter conversation about when work can actually end. The friction is timing—there isn’t enough runway to wait out every slump, yet there’s still enough time that sitting in cash feels like volunteering for inflation.

This is usually when people start scanning for a clean age-based rule, not because it’s perfect, but because it gives them a number they can execute inside a 401(k) by Friday. The catch is that the market doesn’t care about calendars, and the “right” split starts to depend less on age and more on how much loss the plan can absorb without changing the retirement date.

The simple age rule that sounds reassuring

The rule people reach for is usually one subtraction problem: “bond % = age,” or “stocks = 110 (or 120) minus age.” At 60, that lands you around 50/50 or 60/40, which feels calm because it turns an anxious market into an allocation you can set with two clicks. It also fits the practical constraint most plans impose: a limited menu of funds, no time to model scenarios, and a desire to stop tinkering after every ugly week.

As a baseline, the math is doing one sensible thing: it pushes equity exposure down as the retirement date gets closer, which reduces portfolio volatility and the odds that a single bad year forces withdrawals from depressed prices. The trade-off is built in, too. A 60/40 portfolio may not recover as fast after a drawdown, and it may leave less room for inflation surprises if the retirement horizon is 25–30 years. The reassurance comes from simplicity, not from personalization.

The moment that rule fails your real life

The first time the age rule breaks is when you try to map it onto an actual retirement date and an actual spending gap. A 60/40 that looks “responsible” on paper can still be too equity-heavy if you’re planning to leave work in 18 months and your first withdrawals are non‑negotiable (health insurance, bridge to Social Security, a mortgage you don’t want to carry). The rule assumes time is smooth. Real plans aren’t: there’s a narrow window where a 15–25% equity drawdown would force a delayed retirement, not just an uncomfortable statement.

The second break is that age doesn’t measure loss capacity. Two 60-year-olds can have the same balance and radically different risk budgets: one has a pension and flexible discretionary spending; the other is funding nearly everything from the portfolio and can’t cut baseline expenses. Add the common frictions—an employer stock position inside a brokerage account, an IRA that’s mostly equities from old rollovers, or a 401(k) with limited bond options—and the “one subtraction problem” becomes a guess with hidden concentrations.

At that point, the useful question stops being “What’s my age-based split?” and becomes “What loss can I tolerate in the next 12–24 months without changing the date?” That answer is usually smaller than the rule implies.

Set loss boundaries before hunting for return

Once the question becomes “what loss can I tolerate in the next 12–24 months,” the next move is to turn that into a boundary you can actually monitor. Start with the dollars that can’t be exposed to a bad sequence: the first year or two of withdrawals, any known lump sums (roof, car replacement, debt payoff), and the portion of living expenses you can’t cut. If that near-term need is $80,000, then a 20% drawdown on the whole portfolio can’t be “just temporary” if it forces you to sell at the wrong time.

From there, work backward into a maximum acceptable portfolio drawdown—something like 10%, 15%, or 20%—and treat it as a design constraint, not a forecast. A 70/30 allocation might have the return story you want, but if it regularly produces peak-to-trough declines larger than your boundary, it’s the wrong tool for this phase. The point isn’t to avoid volatility; it’s to make sure volatility doesn’t dictate your retirement date.

This is also where cash and high-quality bonds stop feeling “unproductive” and start functioning as a withdrawal buffer. With a boundary in place, the return hunt becomes narrower and more realistic: take equity risk only in the slice that can wait to recover.

Pick your glide path from three realistic choices

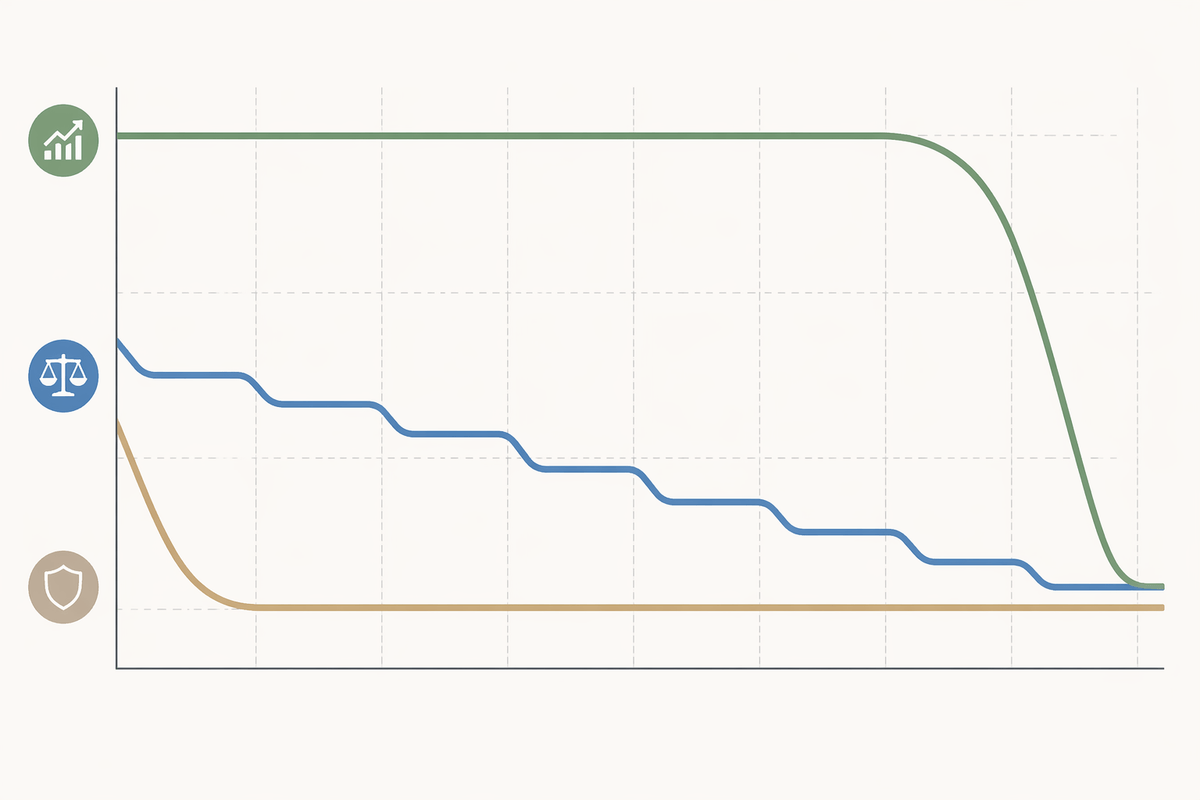

Once you’ve named a drawdown limit that would force a date change, the “right” allocation stops being a single age-based answer and turns into a path you can live with through a bad year. The practical constraint is that you’re not choosing today’s split only; you’re choosing how fast you’ll de-risk over the next decade while contributions fade and withdrawals begin. Three glide paths show up in real portfolios because they match three different tolerances for timing risk—and each has a cost.

The first is a conservative landing: move quickly toward something like 40/60 and hold it. It tends to keep near-term losses inside tighter boundaries, but you pay with lower long-run expected growth and less help against inflation if retirement lasts 25+ years. The second is a balanced slope: sit near 50/50 or 60/40 for a while, then step down in planned increments (for example, every year or two). It’s boring on purpose, and it reduces “one bad year” pressure without freezing the portfolio.

The third is a growth-tilted glide: stay closer to 70/30 until the retirement date is within sight, then build a larger bond/cash buffer for early withdrawals. The appeal is higher expected return; the risk is that a deep equity drawdown arrives before you’ve built the buffer, forcing sales at the worst time.

Make it executable inside your 401(k) and IRA

The nice part about a glide path is that it can be messy behind the scenes and still look clean in one place. If the 401(k) has a decent bond index and stable value, it usually becomes the “buffer” account, while the IRA holds more equity because it has a broader menu. The constraint is taxes and plan rules: you rebalance where trades are free (typically inside retirement accounts), not where they create capital gains or paperwork.

Start by listing every holding by account, then translate it into three buckets: stocks, high-quality bonds/stable value, and cash. If employer stock or an old all-equity rollover is dominating, don’t debate the perfect target—cap the concentration first, then use new contributions to pull the total back toward your chosen slope. Execution beats elegance when the next payroll deposit is the only easy lever.

A yearly reset beats finding one perfect number

What ends up working in practice is treating the allocation as a yearly decision, not a one-time identity. Pick a month, run the same quick checks, and make only the moves that keep the plan inside your loss boundary. The constraint is attention: most people will follow a process they can finish in 30 minutes, once a year, more reliably than a “perfect” glide path they have to babysit.

That reset can be simple: confirm the next 12–24 months of cash/bond buffer, measure whether stocks drifted above the range you intended, and rebalance using the account where trades are easiest. If markets were strong, you’re harvesting risk by trimming. If markets were weak, you’re buying back to the plan instead of chasing reassurance. The number changes; the discipline stays.